In September, we learned that consumer prices in the UK rose by 2.2% in the 12 months to August –...

-

Emerging markets experienced a remarkable surge in September, climbing over 7% in dollar terms, marking their strongest month since November...

Emerging markets experienced a remarkable surge in September, climbing over 7% in dollar terms, marking their strongest month since November... -

In August, we learned that consumer prices in the UK rose by 2.2% in the 12 months to July –...

-

In March 2024, the FCA concluded a thematic review (TR24/1) into retirement income advice. Interestingly, within this review, they found that...

-

In July, we learned that consumer prices in the UK rose by 2.0% in the 12 months to June –...

-

You will have likely woken up to the news that global stock markets have fallen sharply. This appears to be because...

-

You will have seen that the Bank of England (BoE) cut interest rates by 0.25% today, the first cut since...

-

The world of politics took a surprising turn over the weekend, as we learnt that US President Joe Biden has...

-

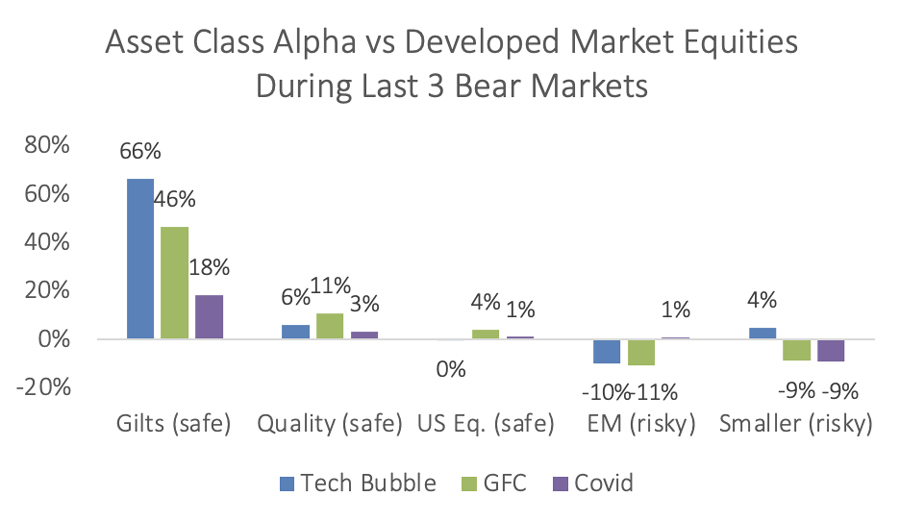

It is conventional wisdom that investment decisions are usually informed by an assessment of the investor’s willingness to take risk...

-

In June, we learned that consumer prices in the UK rose by 2.0% in the 12 months to May 2024,...

-

Following the overnight news that Keir Starmer and the Labour Party won a large majority in the UK General Election,...

-

As one may suspect, we are often among the first companies called by an investment business when a fund manager...

-

In May, we learned that consumer prices in the UK rose by 2.3% in the 12 months to April 2024,...

-

Yesterday, it was announced that the UK will hold a general election on July 4th 2024. We can understand how...

-

The conscious decision to invest in one asset class over another is probably the most important investment decision we will...

-

In April, we learned that consumer prices in the UK rose by 3.2% in the 12 months to March 2024,...

-

You will have likely seen the news on Saturday. On the back of these developments, we noted that equities in...

-

In March, we learned that consumer prices in the UK had risen by 3.4% in the 12 months to February...

-

February saw diverging fortunes in markets, with stocks performing well while fixed income markets were largely down. Within fixed income, it...

-

Chancellor Hunt unveiled this year’s Budget on Wednesday in the House of Commons. Background Since the next UK general election is likely...

-

One of the most common questions we receive from our clients revolves is whether to remain in cash or transition...

-

The “Magnificent Seven” Stocks - Our View and Portfolio Exposure – Fundhouse Adviser Insights6th March 2024The concentration in the S&P 500 of just seven names – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla is...

-

In December, the annual level of UK Consumer Price Inflation rose to 4%, up from 3.9% in November (with a...

-

In November, the annual level of UK Consumer Price Inflation fell to 3.9%, down from 4.6% in October. It is...

-

November saw positive news on inflation – UK CPI data for October fell to 4.6%, a notable drop from 6.7%...

-

On Tuesday, the FCA released a 212-page Policy Statement on Sustainability Disclosure Requirements (SDR) & Investment Labels. These new rules will...

-

On Wednesday, Chancellor Hunt delivered an ‘Autumn Statement’ to give Parliament an economic update and announce new policies – “110...

-

Having seen painful double-digit inflation in late 2022, it was something of a relief in October to see UK inflation...

-

At Fundhouse (UK), we help our clients avoid pitfalls when choosing funds. Fundhouse CIO Joe Wiggins investigates why following the...

-

At Fundhouse, we dig deeper into the data to make better investment decisions for our clients. Have UK equity fund managers...

-

2022 has been an incredibly difficult year for investors. Not only have we seen steep declines in equity markets, but...

-

As a UK citizen, it is certainly worrying that we have our fourth Chancellor and (soon to be) third prime...

-

The UK commercial property market is facing a torrid environment. Not only is the economic outlook bleak; but rising interest...

-

Over the years at Fundhouse (UK), we’ve spoken to dozens of #assetmanagement firms undergoing corporate change. Today, we share insights on...

-

Based on years of observation and bitter, painful experience; here are my thoughts on the ten most significant mistakes made...

-

At Fundhouse (UK), we use our own algorithms to analyse trading patterns, giving our clients greater #investmentclarity about the funds...

-

At Fundhouse (UK), we monitor the fund universe for signs of #liquidity issues, to give our clients better #InvestmentClarity. Today, we...

-

At Fundhouse (UK) we’ve been building a #greenwashing detector to give our clients greater #investmentclarity. We’ve uncovered a number of insights...

-

In today’s blog, we look back at the many meetings that we have had with fund groups discussing ESG. Although...

-

As part of our manager research process for a given fund, we will evaluate the corporate entity employing the investment...

-

In this article, we explore whether there is persistency in tactical asset allocation skill, by evaluating the evidence we have...

-

In this article, we discuss how the historic low yields we are seeing in credit markets today does not seem...