The world of politics took a surprising turn over the weekend, as we learnt that US President Joe Biden has...

-

It is conventional wisdom that investment decisions are usually informed by an assessment of the investor’s willingness to take risk...

It is conventional wisdom that investment decisions are usually informed by an assessment of the investor’s willingness to take risk... -

In June, we learned that consumer prices in the UK rose by 2.0% in the 12 months to May 2024,...

-

Following the overnight news that Keir Starmer and the Labour Party won a large majority in the UK General Election,...

-

As one may suspect, we are often among the first companies called by an investment business when a fund manager...

-

In May, we learned that consumer prices in the UK rose by 2.3% in the 12 months to April 2024,...

-

Yesterday, it was announced that the UK will hold a general election on July 4th 2024. We can understand how...

-

The conscious decision to invest in one asset class over another is probably the most important investment decision we will...

-

In April, we learned that consumer prices in the UK rose by 3.2% in the 12 months to March 2024,...

-

You will have likely seen the news on Saturday. On the back of these developments, we noted that equities in...

-

In March, we learned that consumer prices in the UK had risen by 3.4% in the 12 months to February...

-

February saw diverging fortunes in markets, with stocks performing well while fixed income markets were largely down. Within fixed income, it...

-

Chancellor Hunt unveiled this year’s Budget on Wednesday in the House of Commons. Background Since the next UK general election is likely...

-

One of the most common questions we receive from our clients revolves is whether to remain in cash or transition...

-

The “Magnificent Seven” Stocks - Our View and Portfolio Exposure – Fundhouse Adviser Insights6th March 2024The concentration in the S&P 500 of just seven names – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla is...

-

In December, the annual level of UK Consumer Price Inflation rose to 4%, up from 3.9% in November (with a...

-

In November, the annual level of UK Consumer Price Inflation fell to 3.9%, down from 4.6% in October. It is...

-

November saw positive news on inflation – UK CPI data for October fell to 4.6%, a notable drop from 6.7%...

-

On Tuesday, the FCA released a 212-page Policy Statement on Sustainability Disclosure Requirements (SDR) & Investment Labels. These new rules will...

-

On Wednesday, Chancellor Hunt delivered an ‘Autumn Statement’ to give Parliament an economic update and announce new policies – “110...

-

Having seen painful double-digit inflation in late 2022, it was something of a relief in October to see UK inflation...

-

At Fundhouse (UK), we help our clients avoid pitfalls when choosing funds. Fundhouse CIO Joe Wiggins investigates why following the...

-

At Fundhouse, we dig deeper into the data to make better investment decisions for our clients. Have UK equity fund managers...

-

2022 has been an incredibly difficult year for investors. Not only have we seen steep declines in equity markets, but...

-

As a UK citizen, it is certainly worrying that we have our fourth Chancellor and (soon to be) third prime...

-

The UK commercial property market is facing a torrid environment. Not only is the economic outlook bleak; but rising interest...

-

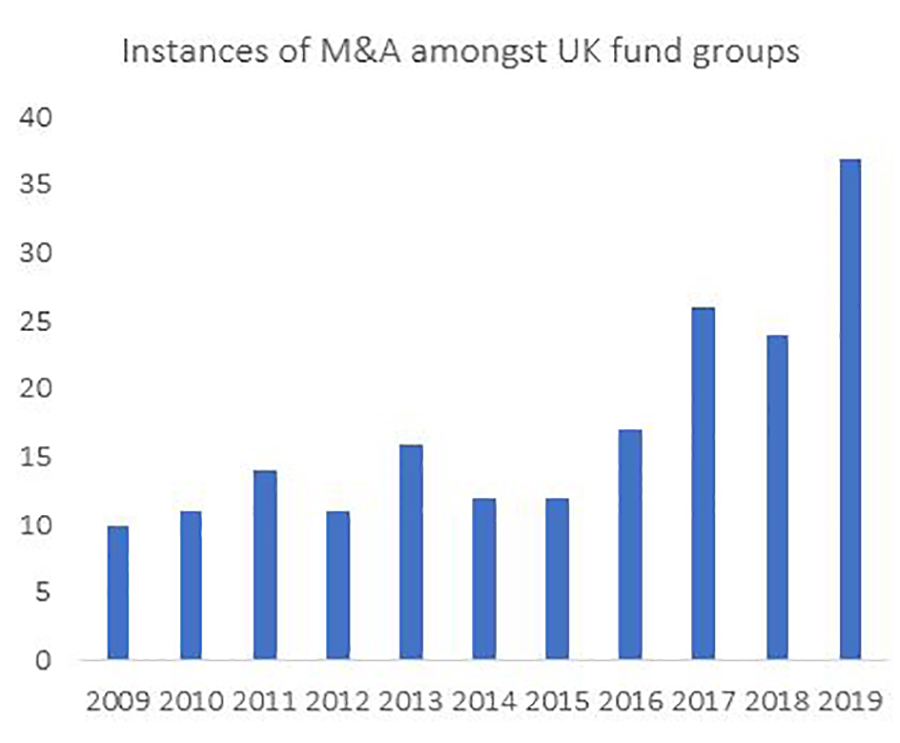

Over the years at Fundhouse (UK), we’ve spoken to dozens of #assetmanagement firms undergoing corporate change. Today, we share insights on...

-

Based on years of observation and bitter, painful experience; here are my thoughts on the ten most significant mistakes made...

-

At Fundhouse (UK), we use our own algorithms to analyse trading patterns, giving our clients greater #investmentclarity about the funds...

-

At Fundhouse (UK), we monitor the fund universe for signs of #liquidity issues, to give our clients better #InvestmentClarity. Today, we...

-

At Fundhouse (UK) we’ve been building a #greenwashing detector to give our clients greater #investmentclarity. We’ve uncovered a number of insights...

-

In today’s blog, we look back at the many meetings that we have had with fund groups discussing ESG. Although...

-

The market has become counterintuitive: in a strongly rising market across almost all asset classes, we find expensive has beaten...

-

In this article, we explore whether there is persistency in tactical asset allocation skill, by evaluating the evidence we have...

-

In this article, we discuss how the historic low yields we are seeing in credit markets today does not seem...